Here's a worthwhile exercise I recently discussed with a trader. Select a measure of market trending, such as a X-period Sharpe ratio for the market. Divide the last couple of years into bullish trending, non-trending, and bearish trending periods. Select a measure of market volatility, such as VIX. Divide the last couple of years into low, medium, and high volatility. Compute your cumulative profit/loss during the bull, non-trending, and bearish periods. Compute your cumulative profit/loss during the low, medium, and high volatility periods. Where are your sweet spots? Where do you lose money? When should you be stepping up your game? When should you be stepping back from markets? Where is your happy zone? Further Reading: Finding Your Trading Strike Zone

.

Interesting research from Daniel Goleman and others suggests that emotional intelligence and social intelligence are important to business leadership. As the graphic above suggests, successful business managers combine self-awareness and self-management with social awareness and relationship management. In other words, effective leaders know themselves and use this awareness to be more effective. They also can read others well and utilize that sensitivity to be more effective with peers. Thanks to a savvy money manager for pointing out this article detailing how social intelligence is much more important in team-based success than IQ. Interestingly, people who are more skilled at reading emotions from the eyes of others are also significantly more effective in teamwork. Women also tend to be more capable at reading the emotions of others than men. One telling predictor of team-based success is the tendency to take turns in talking: effective people speak *and* listen. What are markets but the outcomes of the collective decisions of others? We frequently make reference to market sentiment and changes in market character much as we would speak of another person. Is it such a far stretch to imagine that emotional intelligence helps traders know and manage themselves and social intelligence helps them read and respond to the actions of others? Some of the most successful portfolio managers I know do not engage in copious quantities of original macroeconomic or market research but are quite talented in picking out the best ideas from researchers and other traders. They are like the skilled poker players, who are classically intelligent (they know the odds of each hand); emotionally intelligent (they know their emotions and manage their risk taking); and socially intelligent (they can read the players around the table). All of us have known traders who become so locked in their views they stop seeing and responding to what markets are actually doing. This may masquerade as "conviction", but it is actually socially unintelligent--not unlike harping on a topic in a conversation and alienating listeners. Research finds that social intelligence operates just as effectively in online environments as direct, interpersonal ones. Perhaps one of the boons of social media is the opportunity for traders--including female traders!--to leverage their skills at reading and interacting with others in generating new and better trading ideas.

Two kinds of traders fail to find success: those who cannot change and adapt and those who cannot focus and exploit their edges in markets. Very often traders become frustrated with losses and abandon what they are doing, seeking ever better ideas and methods. This makes it very difficult to ever master any particular opportunity or skill set in markets. Today's best practice submission comes from David Blair (@crosshairtrader). Readers will recognize him from the CrosshairsTrader site and blog. David's best practice is all about focus: eliminating what is non-essential in markets and developing a very specific market edge and expertise:

"When I first started trading I decided to be a sponge, soaking up all the stock market information I could, free or otherwise. After sponging it for a few years I realized I created a monster devoid of creativity; replaced by anxiety, confusion, fear, and impatience, all of which were a result of a lack of focus. I traveled in a black hole with a flashlight and didn't know it.

During these years I was trading with a partner: a friend who introduced me to the business. Each day he would have a new topic for us to study. As a result, our trading room began to look like a war room. 8 monitors, two big screen TVs, 2 color printers for printing charts, cases of books, CDs, seminar manuals, etc. The problem was, the more we added, the worse our performance, the worse our performance, the more we added, creating a vicious cycle of spoiled intentions. As my partner continued to add, I began to subtract. I began practicing minimalism by getting rid of all the things I thought were so important, realizing that stock prices cannot be predicted no matter how much I learned or added to my charts.

My process now involves a very simple, easy to understand price pattern wherein I look for stocks breaking from price boxes to either 1) continue the previous trend or 2) reverse the previous trend. I have a well defined method for locating these trades when they trigger on two time frames, the weekly and daily. I have prepared a watch list of stocks and have developed indicators specifically designed to alert me when there is a potential trade opportunity. In other words, I have become a 'process specialist'. I have developed a specific process that helps me manage the uncertainty of future stock prices. I no longer feel the need to study everything or watch anything other than the stocks on my watch list."

David's methodology makes sense: stocks trading in a box are ones that have consolidated. Both directionality and volatility have gone to reduced levels. He is identifying opportunities in which breakouts place him on the right side of both direction and volatility. This not only means that the market moves his way, but moves his way with impulsivity. Psychologically, having a specific methodology like this reduces distraction and enables a trader to become a true specialist, building skills in a particular kind of trading. Perhaps most important of all, specializing in a type of trading enables David to make trades truly his own, so that he will have the confidence to act--and also has the perspective to quickly recognize when setups are not working.

Many successful physicians are not only specialists but sub-specialists. They find their "edge" by knowing one area in great depth. This can be a very helpful approach for traders as well.

There are several classes of indicators I routinely follow to track market strength and weakness. These include measures of sentiment, breadth, momentum, volatility, correlation, and market participation (behavior of large market participants). Among these measures, there is often considerable statistical overlap. Because they are correlated, they are not truly measuring different things. In an upcoming post, I will address this issue by discussing purified indicators--ones in which overlap has been removed, so that we are looking at purer forms of sentiment, breadth, etc. For an inspiring example of purification, check out this paper from David Aronson highlighting his construction of a purified VIX measure. Above we see three current measures of market breadth. The top chart tracks the sum of 5, 20, and 100-day new highs minus new lows among all shares in the Standard and Poor's 500 Index. The middle chart looks at the average of the percentages of stocks in that index that are trading above their 3, 5, 10, and 20-day moving averages. The raw data for both these measures come from Index Indicators. The bottom chart displays the sum of stocks across all exchanges that are making fresh three-month new highs minus new lows. Note that the three measures tell a similar story: Peaks in breadth tend to precede price peaks for intermediate-term market cycles. Until recently, successive breadth peaks were occurring at fresh price highs for the broad market. During this most recent cycle, we've seen lower peaks in breadth and a failure of breadth strength to generate fresh price highs. All of this is suggestive of a weakening/topping market, as recent buyers have not been able to sustain the market uptrend. Further Reading: Tracking Breadth Across Cycles

.

I recently took a look at changes in the number of shares outstanding of the SPY ETF as a sentiment measure. When traders are bullish, shares are created in the ETF; when they are bearish, shares are redeemed. This is a useful sentiment gauge, because it reflects what traders are actually doing in the market, not just their stated sentiment.

What is interesting is that we have seen considerable share redemption in SPY since the end of the year. Indeed, shares outstanding are down on a 5, 10, and 20-day basis. Since 2012, we've had 23 non-overlapping periods of such share redemption. Ten days later, SPY was up 18 times, down 5 for an average gain of 1.18%, compared with an average 10-day gain of .43% for all other occasions during that period.

Although we are not so far from all-time highs in SPY and have bounced well off recent lows, bearishness on this measure continues. Interestingly, the put/call ratio for all listed U.S. equities has been above .90 for the last two trading sessions, also above average. As noted yesterday, I have concerns about the longer-term pattern of breadth among U.S. stocks. One reason for tracking different market measures is that we can avoid confirmation bias by observing when things are not lining up. Right now, sentiment is not lining up with a picture of a topping market. There are times when flexibility is as important as conviction: a big edge in markets is retaining the option of not trading and waiting for clarity before placing bets. Further Reading: Options-Based Sentiment

.

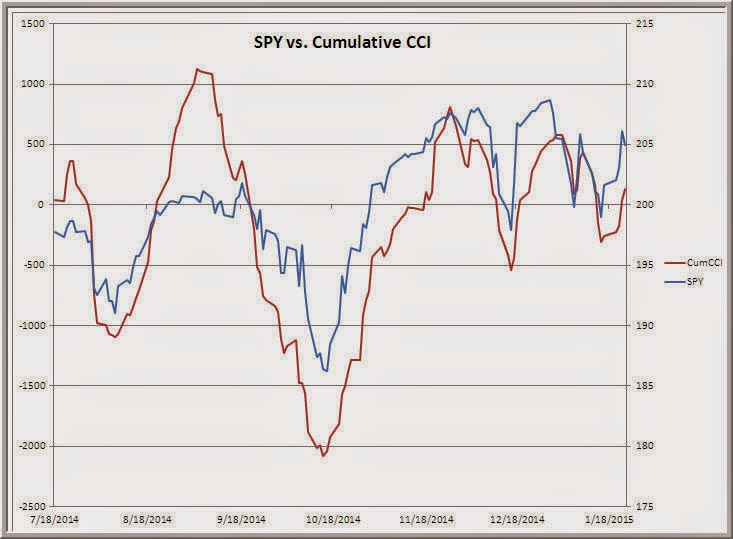

Suppose we think of technical indicators as measures of strength and weakness, with each giving buy and sell signals based upon different time frames and definitions of strength. One way to assess the overall strength of the stock market would be to track, over time, how many shares are giving buy and sell signals across different indicators. The above data track the cumulative buy vs. sell signals for every stock in the NYSE universe based upon the CCI, Parabolic SAR, and Bollinger Bands indicators (raw data and signals via the Stock Charts site). I find it interesting that the cumulative measures have largely lagged price gains since the October lows. This is what I would expect in an environment of weakening stock market breadth. In the wake of dramatic central bank actions this past week, I am watching breadth measures closely to see if the expansion of global QE breathes fresh life into stocks. Further Reading: Tracking Strength With the Bollinger Balance

.

One of the greatest psychological challenges of trading is a cognitive, not an emotional, one. It is the challenge of bandwidth: our limitations in processing large amounts of information at any given time. Many portfolio managers I've worked with have developed ways of expanding their bandwidth, including building out teams to help with research and execution; connecting with savvy peers to discuss market ideas; and staying in touch with colleagues on the trading floor. Turning trading into a team sport increases the number of eyes and ears on markets and is valuable in spotting emerging trading ideas. How many times have I observed traders so focused on their particular trades that they miss what is happening in the broader market? Tunnel vision is a great way to get blindsided in markets.

What social media is accomplishing is a leveling of the bandwidth playing field for individual traders. Most independent traders do not have a trading floor to turn to for market color and cannot afford to build out teams of analysts. Through social media, however, they can turn their trading into a virtual team sport. Cultivating a focused network of insightful peers adds to the eyes and ears on markets and sparks thinking about fresh sources of opportunity. This is why building a social learning network is a best practice in trading. This is a network of peer traders who value your input and provide you with valuable observations and insights into markets. The key to creating an effective social learning network is selectivity. A great deal of the commentary via tweets, blog posts, and chat is high on noise, low on signal. You want a network that provides very high signal value. A great place to start a learning network is Stock Twits. The Stock Twits feed is a curated stream of tweets with high information value. Via the feed, you'll notice certain contributors come up again and again. These are often high value sources of information you will want in your network. Of particular value are the Saturday $STUDY sessions from the Stock Twits feed that select specific tweets and links for their valuable content. In general, the $STUDY postings offer a broad range of observations, analyses, and information. You'll find particular good links via founder Howard Lindzon and head of community development Sean McLaughlin. Yet another place to build your learning network is through sites that comb through content on the financial web and curate selections. Abnormal Returns offers a broad range of links daily and each week selects top podcasts and highlights the most popular links of the week. This also is a great way to discover valuable sources of information that can become your regular listening and reading. On the podcast side, there are the offerings from Michael Covel and Barry Ritholtz that feature interviews with top professionals in finance. Other excellent sources of links are Josh Brown via The Reformed Broker blog and Barry Ritholtz's The Big Picture site. The acid test for any addition to your learning network is that what you read or listen to actually does contribute fresh and useful perspectives to your understanding and trading of markets. There is much to be said for entertainment and it's easy to get into surface readings of many sources, but what is ultimately valuable is what feeds your head. You can't solve fresh puzzles unless you have the right pieces. And you won't get all the pieces if you're locked inside your head. Through social media, you can move from research to building a virtual research team. It doesn't matter how emotionally controlled and disciplined you are: you can't trade the opportunities you never see.

The body's flight or fight response that we know as stress is often a reaction to perceived threat. When we care about an outcome that is uncertain--and especially when we perceive a threat to that outcome--our bodies mobilize for action, with adrenaline pumping, muscles tensing, and heart rate accelerating. That is an adaptive response for dealing with physical threats, such as avoiding an oncoming car, but often gets in the way of careful, deliberate action when the threats we perceive are coming from the trading screen. It is ironic that, just as we most need to be grounded in the rational activities of our frontal cortices, we typically activate our motor areas and risk acting before thinking. How we react to perceived plays an important role in determining whether stress brings distress. Today's best practice comes from Daniel Hunter, who outlines his use of biofeedback in dealing with trading stress. Readers will recognize biofeedback as a tool that I have emphasized both on the blog and in books, as it's a great way for us to become aware of our stress responses and deal with them proactively rather than reactively. Here's what Daniel has to say: "I am a scalper in the forex markets, so anxiety, excitement, and apprehension can creep into the trading day. I combat this with a device that measures heart rate variability. The device I use is the Emwave2. It has an earlobe attachment that I use during trading. I use it along with the computer program provided and have a visual, real time status of my current state. If my emotions start to waver and my breathing starts to change, it alerts me, often before I realize my state. With breathing exercises, I can bring my emotions back under control and focus on what is actually happening in the market. It is also a fantastic practice before bedtime, as you fall asleep faster and your quality of sleep is much improved. It is basically an objective meditation monitor."

Daniel also mentions that considerable research supports the use of heart rate variability feedback in controlling stress and enhancing well-being. Because the monitor gives us real time feedback about whether we are in or out of our performance zone, it serves as a tool for mindfulness. Once we are aware of our stress responses, we can channel them in constructive ways and prevent them from driving our next trading decisions. If we choose to trade, we choose to operate in an environment where there is risk and uncertainty. That ensures that we will experience stress. Our challenge is to turn stress into a stimulus for self-mastery: to control our responses rather than allow them to control us.

In past posts I've mentioned that I track a basket of institutional favorite stocks and monitor upticking and downticking across the group every minute of the trading day. The logic is that when large market participants want to buy or sell with urgency, they will lift offers or hit bids across a range of liquid stocks. This simultaneous upticking or downticking across a range of shares--the execution of buy programs and sell programs--leaves a footprint that provides a very useful view of instantaneous market sentiment.

The top chart tracks sell programs on a rolling one-day basis from October, 2014 to the present. Note the expansion of sell programs at relative market lows and the diminished level of sell programs at relative market highs. That is pretty much what we would expect to see. When we go to the second chart, tracking buy programs, we see the same pattern, however. At relative market lows, we see more buying activity. At relative highs, buying dries up. This is very important. What makes market lows is that lower prices attract longer timeframe buyers--the ones who execute in baskets. Volume ramps up at relative market lows because one group of participants is actively selling and another group is actively scooping up the shares now offered on sale. At relative market highs, nothing is on sale and longer time frame participants are not incentivized to buy. Total volume dries up.

It is the third chart, tracking the relative balance between buying and selling programs, that tells us who is winning the tug-of-war. At market lows, sell programs diminish while buy programs continue to fire. That creates a situation in which buying pressure spikes early in a market cycle. (Note that this is what has happened recently in the wake of the ECB action). As a market rise matures, sell programs begin to exceed buy programs and we see the balance between the two top out ahead of price. The recent significant expansion of program buying suggests that we should see upside momentum from recent central bank actions. I included the fourth, bottom chart to make a separate point. Notice in the third chart how we had intensive selling pressure among the institutional favorite shares prior to the recent market rise. Despite that, the cumulative NYSE TICK (the sum of upticks vs. downticks across all NYSE shares) stayed strong and now has made new highs. What that means is that we were seeing intense selling (downticking) among the liquid large cap issues, but not across the broad market. It was that discrepancy that set up the recent strength. I deeply appreciate the interest readers have shown in the work I have shared. These are proprietary measures (all data from e-Signal and all calculation and charting done in Excel), but I will update periodically to stay on top of where we stand in market cycles. I will also be sharing information about the breadth and sentiment measures I track in my upcoming book. Further Reading: A Look Back on a Previous Instance of Program Buying Surge

.

Think of the successes of great sports teams or businesses. In so many cases, consistency in execution is a common feature. The great football team doesn't just block and tackle well; they do so every play, every game. A business like FedEx or UPS doesn't just deliver on time; they hit their time targets consistently. How can traders achieve high levels of consistency? The answer is by turning trading practices into trading rules. Rules are what turn best practices into habits--and habits are what give us consistency. Contrary to popular conception, discipline is not about forcing yourself to do the right thing. It's about turning right things into habit patterns. Today's best practice comes to us from reader Markham Gross (@MarkhamGross), who is the founder of Anderson Creek Trading, LLC. He explains how the use of rules and systems bring consistency to trading: "A trader or investor cannot control markets or the outside world. All that is under the trader's control is his or her reactions to what is happening in markets or what is perceived to be happening in markets. Therefore, systems should be applied. The best systems are often simple. Spreadsheets can work as an implementation tool and some light programming skills will also go a long way. Systems should be comprised of specific rules for when to enter, exit for loss, exit for profits, and size of the positions. These rules can match the trader's personality and temperament. They should be testable. Although there are limits to backtesting, performing some backtests will help the trader know what to expect so they are not surprised by normal drawdowns. To approach the market without rules on a daily or weekly basis would be a mistake." What I find in my work with traders is that many of the best work in a hybrid fashion: they make decisions on a discretionary basis *and* their decisions are guided by explicit and tested rules. For example, one trader I worked with years ago examined price breakouts that tended to continue in the direction of the breakout versus those that reversed back into the prior range. He found several factors differentiated breakouts from fakeouts, including the volume of the move, where the move stood with respect to longer time frame activity, and the time of day of the breakout. He turned these factors into a checklist, so that he only took breakout trades that scored highly on his criteria. Those rules not only helped him find winning trades, but kept him out of many losers. When that trader first generated the rules, he used the checklist everyday to guide his actions. Eventually, the criteria became solid trading habits and he implemented them routinely. Repetition is the mother of habits and habits are the backbone of discipline. Turning your successful strategies into rules is a great way to ensure that your best practices become robust processes. Further Reading: Success as a Habit

.

Above are two charts from the excellent Index Indicators site that I find useful. The top chart tracks the percentage of SPX stocks making fresh five-day highs. The bottom chart tracks the percentage of SPX stocks making fresh five-day lows. Typically we see five-day highs wane and five-day lows expand as market cycles top out. We also have been seeing five-day lows crescendo ahead of cycle price lows. Yesterday, we closed modestly higher in SPX, but new lows expanded and new highs contracted. Rob Hanna of the insightful Quantifiable Edges service recently issued a query study that noticed downside tendencies when the market rises but the proportion of rising stocks falls short of 40%. Price action during the current market cycle has been somewhat distorted, but I'm viewing the current cycle as having begun with the mid-December lows, having peaked at the late December highs, and now in a down phase. If that is the case, we should see at least one further down leg to the market that would take us below those December lows. A dramatic expansion of new highs would contradict that scenario. Tracking short-term strength/weakness via new highs/lows on a daily and several day basis is a useful way of determining if markets are strengthening or weakening going forward. Further Reading: A Look at Market Cycles

.

Success in trading requires the ability to act decisively in the midst of uncertainty. Even when a trader possesses a durable edge in markets, the random variation around that edge makes for a meaningful proportion of losing trades. Risk management begins with the acknowledgment that we could very well be wrong. Today's best practice, submitted by Jonathan Frank, a 20-year old college student and trader, is the conscious acceptance of uncertainty. Jonathan writes: "The market goes up and down (crazy, I know) and I have been a successful trader because I know that shit happens that you cannot always prepare for, as happens in life. You live, you learn, and you move forward. Once you become okay with this uncertainty, you are ready to hit that buy button. Until then, you might want to start searching for another Albert Einstein" to come up with the perfect theory and prediction of the future. "I assess market uncertainty by educating myself on consumer outlooks, job reports, and international events that have direct and indirect effects on the U.S. markets. I then decide if we are in a state of composure or panic...Market uncertainty is like the weather in that there will always be people speculating about whether stocks are going to go up or down in the future, but unless there is a drastic occurrence you have to be optimistic and know that rainy days are followed by sunshine. Always." Jonathan has not been trading for long, but he has come to an important and mature insight: How we trade depends upon how we assess the environment. Are we experiencing a normal market environment or an abnormal one? If we hear a weather forecast predicting a rain storm, we do not freeze and refuse to go outdoors. We dress appropriately and go about our business, understanding that there is some small possibility that the storm could become something truly ugly and dangerous. If, however, we notice very ominous clouds and very low air pressure and hear a weather alert, we may very well decide to take precautionary measures and batten down the hatches. Jonathan mentions data releases and international events as indicators of uncertainty in the world. In markets, we can also gauge uncertainty by looking at realized and implied volatilities--how much markets are moving and how much volatility is priced into markets via options. I find that historical analyses of markets also provide a useful gauge of uncertainty. When we look at where the market stands today and then go back in time and examine all similar occasions, we can get a sense for the variability of forward outcomes. Sometimes those prospective outcomes contain a directional edge; sometimes they are random. Sometimes those outcomes are highly variable; other times they are more constrained. By examining the uncertainty of past outcomes, we can sensitize ourselves to the uncertainty of the immediate future. Further Reading: Dealing With the Uncertainty of Trading .

* My recent projects have included developing better measures of price momentum and volatility. With respect to momentum, I am working on a measure that cuts across multiple time frames and that measures momentum in vol-adjusted terms. With respect to volatility, I'm working on a measure that cuts across realized and implied vol. Above is a fast measure of multiperiod momentum that has tended to top and bottom ahead of price during intermediate market cycles. Instead of using backtests to predict (and trade) forward price movement, I use the tests as gauges for the average expectable movement from any given configuration of momentum and volatility. That provides a useful framework for determining whether the current market, going forward, is behaving stronger or weaker than average. Sustainable trends, early in their life, perform stronger than average. So far the current market is behaving weaker than average. * Worthwhile perspectives on bond price strength (falling yields) and more from the top links of the week via Abnormal Returns. It's a great way to discover insightful blogs you may have missed. * Does early January performance in the stock market predict full year returns? * A look at market sentiment and what it might mean. * Interesting market observations from Nautilus Research. * A look at returns from trading absolute momentum.

One of the themes of my upcoming book, Trading Psychology 2.0, is that creativity is the new trading discipline. Success in markets is not so much a function as rigidly adhering to a single, unchanging edge as continually finding fresh sources of edge in ever-changing markets. But how do you come up with fresh trading ideas and sources of edge?

Reader, author, and blogger Ivaylo Ivanov (@ivanhoff) offers a best practice that can feed our creativity. Here's what he suggests: Studying your own past trades is a must, but it provides a limited perspective of opportunity cost--it only helps to analyze the trades you took; it tells you nothing about the trades you did not take. One of the most practical habits that has helped me as a trader is going through the daily charts of the best performing stocks on a daily, monthly, quarterly, and 6-month time frame. Here are some of the benefits of this daily exercise: * It has substantially improved my setup recognition skills;

* It has given me ideas for new ways to approach the market;

* It provides an unbiased view of what is currently working in the market; which industries are under accumulation. Recognizing industry momentum is of utmost importance for swing traders as it helps to focus on setups that don't only have higher probability to break out or break down, but are also likely to deliver bigger gains;

* The mere going through the screens provides me with a constant flow of great anticipation swing setups--stocks that are setting up for a potential breakout.

Readers will recognize this as a structured exercise in pattern recognition. In his book, Ivaylo outlines his "perfect setup" for swing trades. His best practice above, additionally enables him to learn new setups. It also allows him to identify sectors that are most likely to yield good setup candidates. Indeed, the patterns that emerge from such review could lend themselves to backtesting and possible systematic inputs into discretionary trading.

I also suspect that Ivaylo's best practice helps him identify market themes early--for instance, the breakdown in energy stocks in the wake of oil weakness or the rise in utility shares resulting from declining global rates. It's not such a leap to go from his exercise to a review of patterns across global markets to identify the macro themes that might be attracting the interest of institutional investors.

Interested readers can check out Ivaylo's website, as well as his book and Twitter feed linked above. He's a great example of savvy traders sharing worthwhile ideas via StockTwits.

The recent post talked about the importance of being mindful of evidence for the other side of your trade and the bounce probability following short-term oversold conditions played out on Friday. Above are three perspectives on the U.S. stock market at week's end. The top chart depicts a ten-day moving average of all stocks across exchanges making three-month new highs vs. lows. That breadth has been deteriorating since late October, but notice also that this week's price lows saw fewer shares making fresh net new lows than at the mid-December bottom. For that reason, I'm viewing the market as a range one defined by the December highs and lows. The middle chart takes a look at the balance between buying pressure (upticks) versus selling pressure (downticks) across all NYSE shares. Note the recent intensity of selling pressure ahead of price lows, followed by Friday's buying surge. This is a pattern that has been common at intermediate market lows and is consistent with the range perspective noted above. Finally, in the bottom chart we see the 10-day average of changes in shares outstanding for the SPY ETF. This has been an excellent sentiment gauge, as we have tended to see expansions in shares outstanding when traders have been bullish and contractions in shares outstanding when traders and investors have been bearish. We finished 2014 with considerable bullishness and recently have swung to the opposite extreme, again consistent with the range notion. The follow through to Friday's rally should tell us a great deal about the vigor of this market. It would be understandable for traders to respond to strength with further buying, given the recent concerns regarding V bottoms. A weak follow through would suggest that recent macro considerations (deflation, global economic weakness) pose ongoing headwinds. I will be tracking that in days ahead. Further Reading: Gaining Fresh Perspectives

.

Consider the talented weather forecaster, the skilled CIA analyst, and the successful sports gambler. What they share is an appreciation of probabilities. It's not that they have a crystal ball into the future. Rather, they are intelligent about the range of possible outcomes and the likelihood of each occurring. In David Apgar's terms, these individuals display risk intelligence. The risk intelligent person is one who quickly learns about risks and rewards and adapts to changes in those. Dylan Evans makes the case that risk intelligence is indeed a distinctive form of intelligence, not correlated with overall IQ. As we sometimes see in markets, very bright people can make very stupid decisions about risk. (See the Projection Point site for an example of a risk intelligence test). Let's take two traders. Both are long a market that has been trending upward. The trend has lasted long enough that the trade has gained popularity and the position is widely held. The first trader cites "price confirmation" and the possibility of a "parabolic" move and increases his position size in the trade. The second trader experiences the same enthusiasm, but looks at positioning, reassesses risk/reward, and buys some inexpensive downside protection with options. When the market stalls and traders run for the exits in the crowded position, the first trader draws down meaningfully. The second trader holds onto the vast majority of gains. *That* is risk intelligence. The first trader is carried away by the market move and becomes risk-stupid. The second trader draws upon risk intelligence to reformulate odds and shift exposure. A great deal of trading success occurs when emotional intelligence--our awareness of our experience and ability to adapt to that--triggers risk intelligence. It's not that successful traders control or eliminate emotions; it's that they use emotions as information in assessing and reassessing risk. The traders I know who have been quite successful sometimes take higher levels of risk, sometimes lower. They are distinguished not by their level of risk taking but by the intelligence of their risk taking process.

In the wake of the decision of the Swiss National Bank (SNB) to end its peg to the euro, we have seen massive volatility in CHF, Swiss stocks, and stocks and currencies globally. Like a flash crash or an unexpected news item or earnings release from a company, such event risk has the potential to inflict significant damage to trading accounts and portfolios.

With the overnight action in the ES futures, my measure of pure volatility--the amount of movement generated by a fixed amount of volume; see chart above--has risen to its highest level since the October lows. The same amount of stock index volume is now generating more than twice as much movement as late in December. What pure volatility tells us is that we don't need specific event risk to see dramatic increases in market movement. During recent market selloffs we've seen both more volume and more volatility per unit of volume.

This is why stress-testing your positions and portfolios is a best practice in trading. Consider the position(s) you currently hold and your intended holding period for that position or positions. Now look back over the past two years of trading and identify the worst drawdowns that could have occurred to that position or portfolio over the course of that holding period. Because financial returns are not normally distributed, the odds of outsized losses are greater than we would expect from usual statistical analyses. Looking back over a period of years and identifying worst possible drawdowns is at least a beginning heuristic to let you know if you could survive a significant event risk or adverse move.

If the loss you would incur from worst case gap/event risks or drawdowns would impair your trading account and impair your trading, you know that your risk-taking amounts to a kind of Russian roulette. It is only a matter of time before an active trader encounters a two-plus standard deviation adverse move. Sizing positions to survive stress tests is immensely important to longevity in a trading career.

Sizing is not a total solution, however. Even reasonable sizing wouldn't have protected you from the kind of multi-multi standard deviation move we just saw in the Swiss franc. This is why diversification in a portfolio is essential. When one position blows out, other positions have the opportunity to work in your favor. Spreading risks that are sized properly helps protect traders and investors from those rogue moves that are associated with fat tails of financial returns. You can't win the game if you can't stay in the game. The trading literature is filled with admonitions to size up trades and portfolios when you have confidence in your views. Flash crashes happen. Downside gaps on negative earnings surprises happen. Spikes in volatility happen. Confidence not tempered with prudence is an accident waiting to happen. Further Reading: Mistakes in Risk Taking

.

The recent look at the market suggested weakening breadth in a market dominated by deflation concerns. Interestingly, stocks have traded lower and we're starting to get into negative territory on the intermediate-term strength measure (above). That measure takes the number of SPX stocks making fresh 5, 20, and 100-day highs vs. lows and smooths those with a ten-day moving average. The indicator has room to go on the downside to be sure, but I do make note that we're hitting levels similar to those seen in December even though prices remain higher. When weak breadth cannot produce fresh price lows, I become more vigilant for the possibility of a bounce higher. On a related note, I have mentioned in the past the Stock Spotter site of John Ehlers and Ric Way. They make use of cycle analysis to generate buy and sell signals for individual stocks and ETFs. Notably, they publish their track record of signals and have done well overall. I note that, as of yesterday's close, they had 138 buy signals on stocks. Since late 2013, when I began tracking the service, there have only been five occasions in which we've had 100 or more buy signals. It's a small sample, to be sure, but all five occasions were higher in SPY five trading sessions later, by an average of 1.59%. Indeed, when we divide the buy signals by quartiles and look at the highest quartile (most buy signals), we see an average next three-day gain in SPY of +.33%. The lowest quartile (least buy signals) yields an average next three-day gain in SPY of +.06%. This is clearly not how John and Ric designed the service to be used, but I do find it interesting that the broad market has tended to perform best when individual stocks are giving the greatest number of buy signals.

The key point is that, even when you have a strong directional view on a market--especially when you have a strong directional view on a market--it is valuable to avoid confirmation bias and seek out information that runs counter to your conviction.

Perhaps this is the most important performance principle of all: We internalize what we do repeatedly. When we engage in behaviors again and again, those behaviors become a habitual part of us. That can work for better or for worse. It's an expression of the idea of "use it or lose it". Our capacities never stay constant. We either develop them or let them atrophy. What we develop defines who we are. This is why negative thinking is so damaging: over time we internalize a negative sense of self. It's also why it's important to develop ourselves cognitively, physically, emotionally, and spiritually. Each day, each week, we either exercise those capacities or we lose just a bit of life fitness. What are the success behaviors you repeat day in and day out? What are you exercising regularly and what has been going undeveloped? Can we really expect to internalize a sense of success when we're not succeeding at the daily challenges we define for ourselves? Here's an excellent resource from James Clear on building positive habit patterns.

Who we are is an internalization of what we do. Life is one big gym and each day is a potential workout. What will you develop today?

I have consistently found that success comes from asking better and deeper questions. It's the out of the box questions that can lead to fresh insights and answers. I recently came across a 2014 review of performance from a trader that outlined all the mistakes he had made during the year and the things he wanted to improve. I asked a question he did not anticipate: "What did you do well in 2014 and what if you *only* did those things in the new year?" Asking a fresh question will not always generate new and better answers, but asking the same, stale questions almost certainly will not yield creative insights. In my current research, I'm looking at overbought and oversold indicators. How much of an edge do they actually provide? Do some measures offer significantly greater edges than others? Over what time frames? Do overbought and oversold measures offer different levels of edge in different types of markets? Are there times to utilize these indicators and times we should not be giving them weight? Notice that such an approach is very different than simply looking at a standard measure such as RSI or Stochastics and pronouncing a given level as overbought or oversold. It's the tougher, more detailed questions that can yield nuggets of insight. For example, suppose we track the number of stocks in the SPX index that are making fresh five-day highs vs. five-day lows. If we go back to 2006 and divide the market into quartiles based upon volatility (VIX), we find that an oversold level in the lowest VIX quartile (1 SD below average) is -62. An oversold level in the next VIX quartile is -138. In the third VIX quartile, the same oversold level is -199. And at the highest VIX quartile, the oversold level is -265. In other words, what constitutes overbought and oversold is relative to the volatility regime of the market. Looking at static levels of overbought and oversold across all markets gives us very distorted results. Does a regime-specific measure of overbought vs oversold breadth offer a greater trading edge than an absolute level? It's all very testable, but only if we gather the data and ask the question. Further Reading: Institutional Participation and Momentum

.

* The recent post illustrated the deflation theme impacting global stock markets. My concern is that the overseas weakness may be more subtly impacting U.S. stocks. The top chart tracks stocks across all exchanges and the number making fresh three month new highs vs. lows. Note that the balance of new highs vs. lows has been waning since the very end of October. The bottom chart tracks all NYSE shares closing above their upper Bollinger Bands vs. those closing below their lower bands. This measure also has been showing waning upside strength. This invites the hypothesis that the recent market action represents a topping process and that we could see a meaningful leg lower as the result of any oil/commodity-led capitulation. * Interesting post on why the Fed may be concerned about overseas economic weakness. See also why deflation may be relevant to China and why "lowflation" is a challenge for Europe. * Some excellent links from the past week via Abnormal Returns, including the asset that best diversifies a stock portfolio. * Thanks to Steve at SMB for pointing out this well researched book and resource on momentum investing. Have a great start to the week! Brett

The broad U.S. stock market (New York Stock Exchange Composite Index; top chart) has been making lower highs, but other equity markets have been in significant decline since mid-year, including EuroStoxx (FEZ; second chart from top); non-U.S. shares (EFA; third chart from top); and emerging markets (EEM; third chart from bottom). At the same time, we've been seeing a precipitous decline in oil prices (USO; second chart from bottom) and dramatically declining yields at the long end (TLT; bottom chart). A common theme among these markets is deflation. My concern is that a capitulation leg down in oil from here would lead to a similar risk-off leg among stock markets, including the U.S., reflecting concerns regarding possible global recession. An update on the breadth and other indicators will expand upon this idea. Further Reading: The Challenges of Disinflation

.

Deliberate practice is a process in which we continually evaluate performance and use those evaluations to make targeted efforts at improvement. Research from Anders Ericsson and others suggests that deliberate practice is essential in developing performance expertise. Today's best practice comes from reader Norbert Beckstrom and consists of a daily review of trading performance. The power of such a review comes from the fact that it can anchor a process of continuous learning and performance improvement. Here are the questions Norbert puts to himself after a day's trading: 1) Did I put on high probability (A+) trades that I wouldn't be easily scared out of? 2) Did I trade to win or did I trade not to lose? 3) Did I have enough size in my conviction trades? 4) Did I break any of my rules? Why? 5) Was I mindful of what I was doing? 6) How many of today's trades would I make again under the same circumstances? 7) How many of my trades did I bail on before the stop or profit target? How did that work out? 8) How many of my trades today were placed out of fear of missing a move? 9) How many trades did I miss today because I wasn't paying attention or was working on something else? 10) How many doubles were there that I didn't have an edge for? 11) How do I feel about my trading at the end of the day? 12) What can I do to improve these answers? Norbert adds that if he conducts this review in the morning before the market open rather than in the evening at the end of the trading day, the answers are more likely to be fresh in his mind and he's more likely to avoid making trading mistakes. In that sense, his review process is a mindfulness process. Clearly, Norbert's review is geared to a discretionary day trader. Traders with different trading styles and traders working on different trading issues will have very different review lists. My review, for example, is much more about markets and much less about making emotional errors. Because my trades are based upon backtested rules and relationships, my first hypothesis is that a losing trade means I may well have missed something important and idiosyncratic in the market. This prods me toward further market analysis. Should the trading loss result from not following my rules, that would prod me toward further self analysis. Ultimately, the most important question is Norbert's final one. Answering the questions is only useful to future performance if the answers anchor specific plans and actions toward improvement. Review is necessary for deliberate practice, but not sufficient. It is what we *do* with the answers to our review questions that determines whether our experience turns into learning and development. Further Reading: The Rage to Master

.

Author of The Psychology of Trading (Wiley, 2003), Enhancing Trader Performance (Wiley, 2006), The Daily Trading Coach (Wiley, 2009), Trading Psychology 2.0 (Wiley, 2015), The Art and Science of Brief Psychotherapies (APPI, 2018) and Radical Renewal (2019) with an interest in using historical patterns in markets to find a trading edge. Currently writing a book on performance psychology and spirituality. As a performance coach for portfolio managers and traders at financial organizations, I am also interested in performance enhancement among traders, drawing upon research from expert performers in various fields. I took a leave from blogging starting May, 2010 due to my role at a global macro hedge fund. Blogging resumed in February, 2014.