Friday, April 15th

* Adam Grimes offers perspectives on mastering trading fears. It's one reason risk management is so important. If losses become emotionally debilitating, they inevitably result in future poor trades and missed opportunities.

* Stocks traded in a slow, narrow range yesterday. Breadth tailed off a bit, but fresh monthly highs continue to significantly outnumber new lows: 1009 vs. 110. About 65% of SPX stocks closed above their three-day moving averages, down from over 85% yesterday. If the recent move to new highs was indeed a breakout move, we should see upside follow through and decent volume on such a move. Stalling on slow volume gives me pause. A false breakout would trap a lot of late bulls.

* We continue to see an increase in shares outstanding for the SPY ETF. That has led to subnormal near-term returns in SPY on average; it's a useful sentiment gauge.

* Recent sessions have shown a notable absence of selling pressure from institutions on the upticks/downticks measure. As long as that's the case, it's difficult to imagine much of a correction in stocks. Conversely, an expansion of downticks (selling pressure) would be an early sign of potential regime shift.

Thursday, April 14th

* More must reading each week: Why earnings expectations are important and great weekly summaries from Dash of Insight.

* Stocks moved to new rally highs yesterday with solid breadth. Across all exchanges we had 1084 monthly new highs against 119 new lows, the strongest reading since late March. While the new highs aren't quite as strong as readings last month, the relative absence of shares making new lows is telling. The market generally makes significant reversals from highs when individual sectors break down. I'm not seeing that breakdown so far.

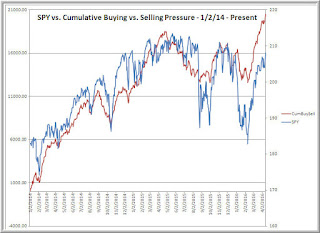

* Another perspective can be found in the cumulative number of buy signals versus sell signals among all NYSE stocks across multiple technical indicators (see below). During 2015, this measure trended lower as groups of stocks failed to participate in market strength. Now we can see it trends higher.

* At a more micro level, cumulative upticks versus downticks among NYSE shares also continues quite strong. This measure often trails off when we see weakness among smaller cap shares. I'm not seeing that weakness at present.

* All that being said, a number of my measures are stretched to the upside now (over 90% of SPX shares closed above their 50-day moving averages and over 80% above their 3 and 5-day averages), so it wouldn't be unusual to see some consolidation. Note that pullbacks in breadth (below) have occurred at successively higher price lows.

Wednesday, April 13th

* Every day I'll try to identify a particularly good reading pertaining to markets. This will also help to highlight people doing good work. Here's an unusually thought-provoking post on stock market valuation from David Merkel at Aleph Blog.

* Stocks traded steadily higher yesterday on the heels of positive oil news. We've since added to those gains in premarket trading and look to test recent highs. Interestingly, breadth is lagging a bit here. Across all exchanges, fresh monthly new highs dropped from 598 to 577 and new monthly lows rose from 281 to 332. Here's how the three-month new highs vs. lows look at this juncture:

* Buying interest continues to swamp selling pressure on the upticks/downticks measure. The cumulative ticks have broken to a new high (see chart below) and institutional participation (total upticking and downticking) has been strong. That has led to positive near-term returns on a short-term basis.

* Since March 21st, we've seen net share creation in the SPY ETF, one of my favorite sentiment measures. Returns have tended to be best when we've seen net redemptions.

Tuesday, April 12th

* Some excellent wisdom in the Abnormal Returns interview with Matt Hall, including making investing and trading fit into your life and not the reverse.

* Stocks finished with a late selloff after early strength and have since bounced a bit higher in overnight trade. Bottom line is that we continue in a range trade. Despite the selloff, advancing stocks outnumbered declining shares. New monthly highs across all exchanges rose to 598 and monthly lows dipped to 281. About 50% of SPX shares closed above their 3-day moving averages and 46% above their 20-day averages--the kinds of numbers you might expect in a range market.

* Year to date, as the graphic from FinViz suggests, we've seen strength among utility and basic material shares (falling rates and the bounce in commodities have helped) and weakness among financial and healthcare shares. It's been a bull market for some sectors and bearish for others--quite a mixed performance.

* US dollar weakness has corresponded to the period of higher commodities and higher prices for overseas stocks as well as US ones. At some point dollar weakness will become overpositioned to the point where we could see a meaningful unwind; that would be a potential risk-off scenario to be on the lookout for. We're having trouble sustaining weakness as long as a weak dollar helps global economies.

Monday, April 11th

* You're running your trading in a smart way, but are you running it in an emotionally intelligent way?

* We continue to trade in a range, as stocks on Friday generally closed higher but off their lows. As of Friday's close, we saw new monthly highs expand from 385 to 476 and fresh monthly lows drop from 517 to 295. That 517 new monthly lows was the weakest reading we've seen since the uptrend launched in February; I'm watching carefully to see if it holds. Significantly fewer than 50% of stocks closed on Friday above their 3, 5, and 10-day moving averages. (Data from Index Indicators). I would be concerned for the bull trading case if we cannot sustain a bounce from here.

* Commodity-related shares (XLB, XLE), consumer staples (XLP), and healthcare (XLV) have been relatively strong in recent sessions; retail (XRT) and financial (XLF) shares have been relatively weak. Note the particular relative weakness of regional banks (KRE) and the continued crushing of yields in the Treasury (TLT) and high quality corporate (LQD) areas. The banking sector index ($BKX) looks anemic. If we were to have problems unraveling the bull, my vote goes to the banking group.

* Continued concerns about pension shortfalls are in the media. One person is quoted as saying that 7+% annual returns over the long haul are reasonable for pension fund payout assumptions. Reminds me of assurances about ongoing 7% growth in China, even as outflows continue. In a world of crushed yield, it seems to me pension funds cannot achieve targeted returns without enhanced risk-taking. That is scary.

* Across a range of technical systems, we've seen a tailing off of buy signals relative to sells, with the two about even as of Friday's close.

* Adam Grimes offers perspectives on mastering trading fears. It's one reason risk management is so important. If losses become emotionally debilitating, they inevitably result in future poor trades and missed opportunities.

* Stocks traded in a slow, narrow range yesterday. Breadth tailed off a bit, but fresh monthly highs continue to significantly outnumber new lows: 1009 vs. 110. About 65% of SPX stocks closed above their three-day moving averages, down from over 85% yesterday. If the recent move to new highs was indeed a breakout move, we should see upside follow through and decent volume on such a move. Stalling on slow volume gives me pause. A false breakout would trap a lot of late bulls.

* We continue to see an increase in shares outstanding for the SPY ETF. That has led to subnormal near-term returns in SPY on average; it's a useful sentiment gauge.

* Recent sessions have shown a notable absence of selling pressure from institutions on the upticks/downticks measure. As long as that's the case, it's difficult to imagine much of a correction in stocks. Conversely, an expansion of downticks (selling pressure) would be an early sign of potential regime shift.

Thursday, April 14th

* More must reading each week: Why earnings expectations are important and great weekly summaries from Dash of Insight.

* Stocks moved to new rally highs yesterday with solid breadth. Across all exchanges we had 1084 monthly new highs against 119 new lows, the strongest reading since late March. While the new highs aren't quite as strong as readings last month, the relative absence of shares making new lows is telling. The market generally makes significant reversals from highs when individual sectors break down. I'm not seeing that breakdown so far.

* Another perspective can be found in the cumulative number of buy signals versus sell signals among all NYSE stocks across multiple technical indicators (see below). During 2015, this measure trended lower as groups of stocks failed to participate in market strength. Now we can see it trends higher.

* At a more micro level, cumulative upticks versus downticks among NYSE shares also continues quite strong. This measure often trails off when we see weakness among smaller cap shares. I'm not seeing that weakness at present.

* All that being said, a number of my measures are stretched to the upside now (over 90% of SPX shares closed above their 50-day moving averages and over 80% above their 3 and 5-day averages), so it wouldn't be unusual to see some consolidation. Note that pullbacks in breadth (below) have occurred at successively higher price lows.

Wednesday, April 13th

* Every day I'll try to identify a particularly good reading pertaining to markets. This will also help to highlight people doing good work. Here's an unusually thought-provoking post on stock market valuation from David Merkel at Aleph Blog.

* Stocks traded steadily higher yesterday on the heels of positive oil news. We've since added to those gains in premarket trading and look to test recent highs. Interestingly, breadth is lagging a bit here. Across all exchanges, fresh monthly new highs dropped from 598 to 577 and new monthly lows rose from 281 to 332. Here's how the three-month new highs vs. lows look at this juncture:

* Buying interest continues to swamp selling pressure on the upticks/downticks measure. The cumulative ticks have broken to a new high (see chart below) and institutional participation (total upticking and downticking) has been strong. That has led to positive near-term returns on a short-term basis.

* Since March 21st, we've seen net share creation in the SPY ETF, one of my favorite sentiment measures. Returns have tended to be best when we've seen net redemptions.

Tuesday, April 12th

* Some excellent wisdom in the Abnormal Returns interview with Matt Hall, including making investing and trading fit into your life and not the reverse.

* Stocks finished with a late selloff after early strength and have since bounced a bit higher in overnight trade. Bottom line is that we continue in a range trade. Despite the selloff, advancing stocks outnumbered declining shares. New monthly highs across all exchanges rose to 598 and monthly lows dipped to 281. About 50% of SPX shares closed above their 3-day moving averages and 46% above their 20-day averages--the kinds of numbers you might expect in a range market.

* Year to date, as the graphic from FinViz suggests, we've seen strength among utility and basic material shares (falling rates and the bounce in commodities have helped) and weakness among financial and healthcare shares. It's been a bull market for some sectors and bearish for others--quite a mixed performance.

* US dollar weakness has corresponded to the period of higher commodities and higher prices for overseas stocks as well as US ones. At some point dollar weakness will become overpositioned to the point where we could see a meaningful unwind; that would be a potential risk-off scenario to be on the lookout for. We're having trouble sustaining weakness as long as a weak dollar helps global economies.

Monday, April 11th

* You're running your trading in a smart way, but are you running it in an emotionally intelligent way?

* We continue to trade in a range, as stocks on Friday generally closed higher but off their lows. As of Friday's close, we saw new monthly highs expand from 385 to 476 and fresh monthly lows drop from 517 to 295. That 517 new monthly lows was the weakest reading we've seen since the uptrend launched in February; I'm watching carefully to see if it holds. Significantly fewer than 50% of stocks closed on Friday above their 3, 5, and 10-day moving averages. (Data from Index Indicators). I would be concerned for the bull trading case if we cannot sustain a bounce from here.

* Commodity-related shares (XLB, XLE), consumer staples (XLP), and healthcare (XLV) have been relatively strong in recent sessions; retail (XRT) and financial (XLF) shares have been relatively weak. Note the particular relative weakness of regional banks (KRE) and the continued crushing of yields in the Treasury (TLT) and high quality corporate (LQD) areas. The banking sector index ($BKX) looks anemic. If we were to have problems unraveling the bull, my vote goes to the banking group.

* Continued concerns about pension shortfalls are in the media. One person is quoted as saying that 7+% annual returns over the long haul are reasonable for pension fund payout assumptions. Reminds me of assurances about ongoing 7% growth in China, even as outflows continue. In a world of crushed yield, it seems to me pension funds cannot achieve targeted returns without enhanced risk-taking. That is scary.

* Across a range of technical systems, we've seen a tailing off of buy signals relative to sells, with the two about even as of Friday's close.